BlogCast #5: Spotlight on Check Point stock

5May23 $CHKP Audio+Transcript+Charts

Summary

John discusses his recent recommendation, where he added to his position on Check Point stock, highlighting the company's consistent earnings growth, strong financial position, and expertise in the growing cybersecurity industry. He believes the stock is currently undervalued, making it an attractive long-term investment.

Audio Here’s a synthesized audio playback of the Purple Chips call between Raymond and John. You can adjust the playback speed.

Transcript of BlogCast on Check Point stock

Moderator: Welcome to our Purple Chips blogcast. Charts are included after the transcript that you may wish to refer to.

Raymond: Good morning, John.

John: Hi Raymond.

Raymond: I see that we recently made a purchase of Check Point stock, and I was hoping we could talk about that on this broadcast. So, what's happening? Why did we buy the stock?

John: First of all, we already owned Check Point before we bought it, and we had a 2.63% holding in this stock. However, that's a little less than our usual overweight position, which should be at 3.75%. This was an opportunity to add to the stock at a bargain price.

Now, let's go into the details of why the stock dropped. We bought the stock on May 1, adding to our position at $120.46. Today, on May the fourth, the stock is trading at $120.40, within pennies of where we bought it. They released earnings, and while the overall earnings picture was good, revenues were lower than expected. The stock dropped from about $127 to around $122 at the open, and some analysts lowered target prices.

Despite this, we decided to add to our position because Check Point is a fantastic stock. The company has not had a single declining quarter in the last 20 years, a remarkable achievement demonstrating its superior quality. The earnings have continuously risen, and we expect this to continue.

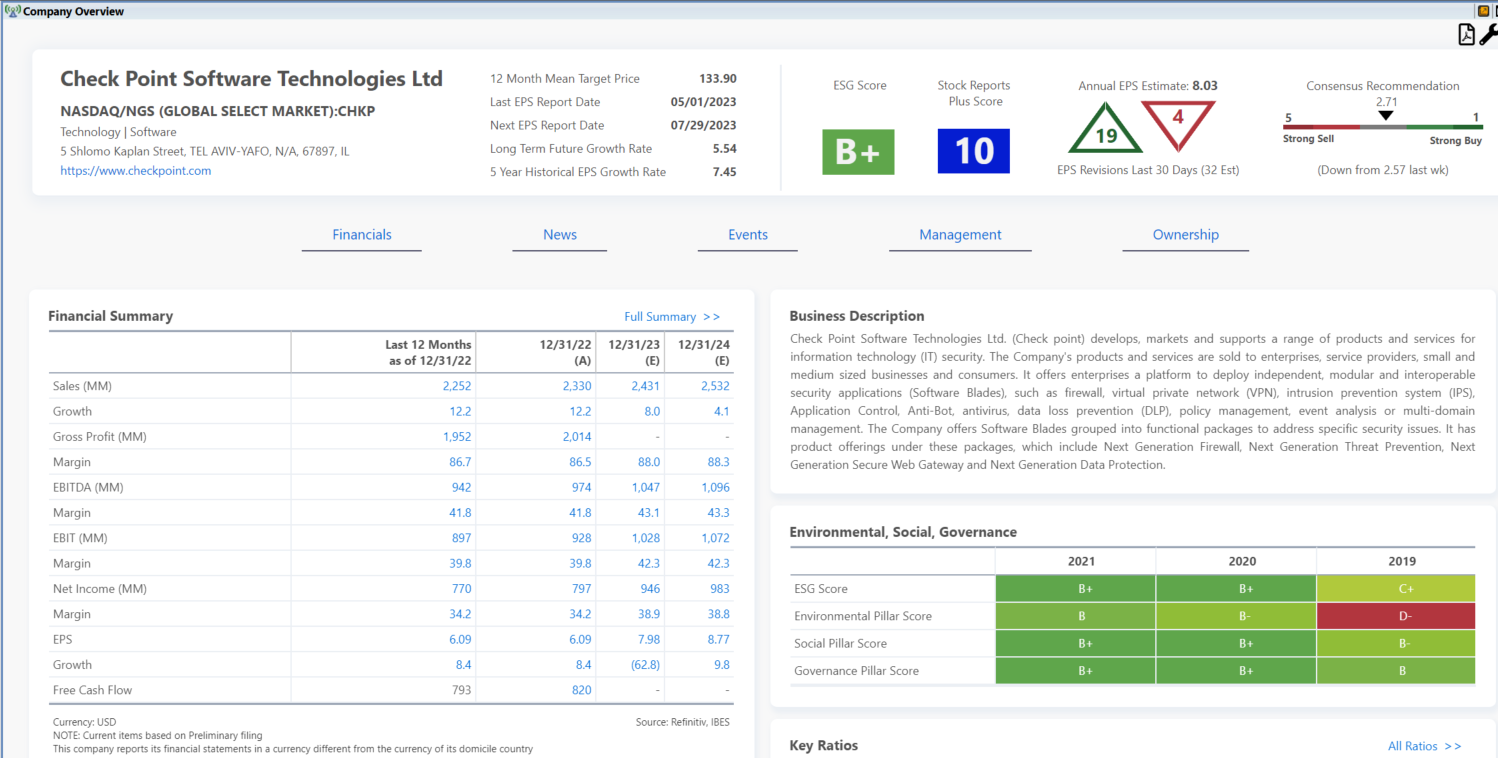

In the last 12 months, the stock has been undervalued a few times, and we believe it's currently in the bargain bin. We have assessed the stock's valuation from three perspectives: fair, low, and high. The stock, as it currently stands, is around $120 to $121. A fair valuation for Check Point would be closer to $135. A high valuation would be in the range of $145 to $150. The Stock Report score is a 10, the highest rating for quality, and the ESG score is a B+.

Another important factor is the company's cash on hand. With interest rates rising, Check Point's $1.6 billion in cash and no debt make it well-positioned to weather any challenges brought on by rising interest rates. The company operates in the growing cybersecurity industry, protecting against increasing cyber threats as the world becomes more digital. We anticipate consistent earnings growth for the next few years, given Check Point's excellent track record.

I'd also like to emphasize the importance of the cybersecurity sector in which Check Point operates. As our society becomes more dependent on technology, the need for robust cybersecurity solutions will only grow. Check Point's expertise in this field, along with its impressive track record, makes it a strong player in a market with significant growth potential.

Moreover, considering the current economic climate, Check Point's financial strength and cash position are even more critical. Companies with healthy balance sheets are better equipped to navigate any economic turbulence and maintain stability for their shareholders. This, in turn, makes Check Point an attractive long-term investment.

Raymond: Thanks, John, for that comprehensive analysis.

John: My pleasure.

Charts

Earnings always improving over the last 20 yrs

Ratings: ESG B+, Stock Reports Plus : 10 (out of 10)

Cash in Bank: $1.6B

Earnings Outlook:

Short and weekly broadcast suits me well. Thanks.